Three years in a row of double digit returns in the equity markets has a lot of investors wondering when they should start to trim or sell their winning positions. As we inch closer to the end of the year, these positions carry with it not just potential liquidity, but also a presumed capital gain once they are sold.

Every year, usually April 15th (or October for those filing extensions) the Government comes calling for their cut of what you’ve made through your income or other sources.

The goal of this piece is to better educate you on your options around these potential tax conflicts, what to look out for, how to mitigate, lower, defer, or at least control your tax liability.

With all that, I am not a CPA or Tax Advisor,all of what is discussed here, although factual, should not be taken as individual tax advice.

Capital Gains Primer

Not everything you buy will go up in value, for the purposes of this, we are only focusing on when things go up from the time you buy them, to the time you sell.

If the asset you bought has increased in price,when you sell, you will have a realized gain. Determining how much tax you owe depends on how long you have been invested. If you bought something less than 1 year ago, the gain is characterized as a short-term capital gain, and after 1 year that gain would be treated as a long-term capital gain.

This difference is key in how you will be taxed on the gain. Any short-term gain will be added to your ordinary income, which is typically taxed at a higher rate than long-term capital gains. Your long-term capital gains are taxed based on your income, but fall into buckets of 0%, 15%, or 20%.

So, for anyone in a higher tax bracket, your ordinary income may be 32% or higher, where as that same individual would be taxed at 20% on the same gain amount, just for making sure that you note how long you’ve held something from the time you bought it.

**There are a lot more nuances to capital gains, your individual and unique tax bill, so please make sure to speak with a professional CPA or tax advisor for any specific questions.

How To Mitigate Taxes

It is impossible to avoid death, as healthy as we can be ultimately when our time is up our time is up. Similarly with taxes, you can avoid paying taxes as long as you want, but ultimately the IRS and government will get theirs; plus, it is not exactly legal.

So, if the goal is to invest and have your account go up, but ultimately use those funds to spend, buy something else, etc. how can you make sure you are as efficient as possible when minimizing your tax bill and keeping more of your earned value.

Let’s go through a few ideas and strategies.

Gifting

This is a good strategy, although it doesn’t really give us all the benefits we may desire. So how does this work?

Let’s say you have a stock that you bought over a year ago and it has gone up significantly since then. You could set up a Donor Advised Fund and give some, or all the shares of that stock, to the Donor Advised Fund. This allows you to get a tax deduction on the full market value of the gift, up to a certain percentage of your AGI in that calendar year.

The Donor Advised Fund sells the stock without a capital gain, and then you can use those proceeds to fund various philanthropic causes that come up during the year and for future years.

Many charitable organizations also can receive stock into their own Donor Advised Funds that they have set up, which eliminates your need to set up your own. Either way it is a good strategy for minimizing your taxes on a stock that has gone up in your portfolio.

However, the funds in the Donor Advised Fund have to go to a charity of some sort and cannot be used for a new car or other personal expenses you may want to use your stock price appreciation for.

Section 351 Exchange

Many Real Estate professionals are familiar with 1031 exchanges where you sell one property at a gain, and roll those proceeds into a new home, deferring the tax bill and not having to pay it immediately since the proceeds were put into a new Real Estate property within the appropriate amount of time.

Similar to these, we now have a tax deferral strategy for stocks to diversify or at least defer your tax bill.

A section 351 exchange is a tax-deferral strategy where you transfer stock that has appreciated into a section 351 fund. Once inside the fund, or ETF, the position(s) are sold, and the proceeds are invested in a diversified strategy which helps improve the original concentration risk of the single position.

There are a few requirements for a section 351 exchange to be mindful of for it to work. The investor, or group of investors, that transfer assets into the fund or corporation must maintain at least 80% of the voting stock in the fund or corporation.

Additionally, to eliminate an investor from just sending over one stock that went up a lot to defer taxes, the IRS made diversification rules. These rules are that no single security can exceed 25% of the portfolio’s value and the top five holdings cannot be more than 50% of the portfolio.

Let’s say all the criteria are met, then what happens? You get shares, with a costbasis, of a new diversified portfolio that will defer your taxes.

But that brings us back to the original question here, you wanted to spend your proceeds on something personal, this does not really help with that since selling out of your section 351 fund would still be taxed at a similar gain as the original stock, even though it is a more diversified portfolio.

Tax Loss Harvesting

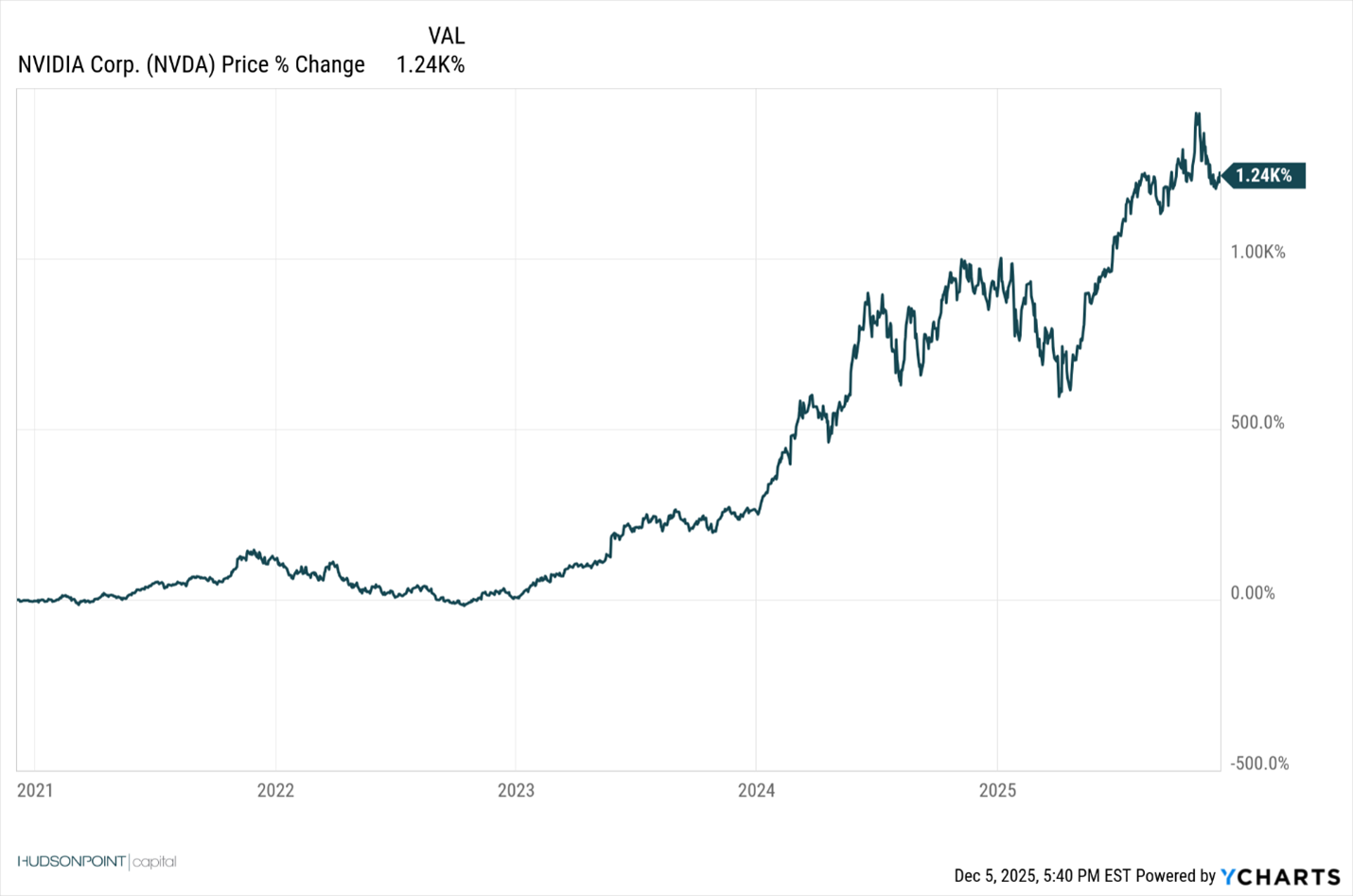

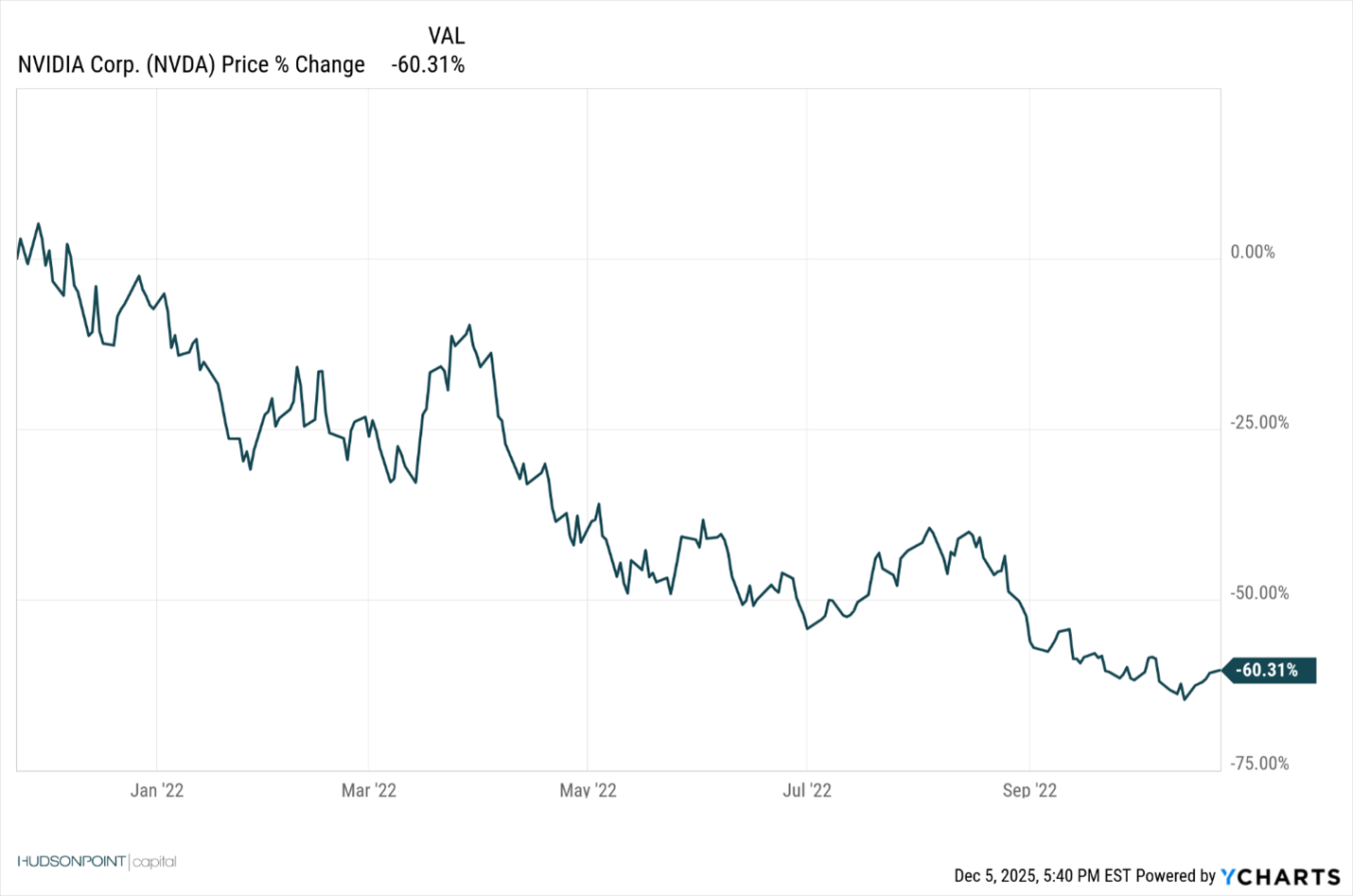

We can look at any individual or stock market index chart to see that even stocks that have gone up a lot, do not always go up in a straight line, see the NVIDIA chart from the past 5 years below.

Even a stock like this that has a 5-year return over 1,200% was, from peak to trough in 2021 into 2022, down over 60%.

Tax loss harvesting, conceptually takes advantage of this inherent volatility in the stock market.

There are newer iterations of this strategy so let’s look at a few.

First, let’s say you bought a stock and just timed it badly. As soon as you bought it, some news came out and the stock went down. You still believe in the long-term vision of the company but cannot stand seeing the unrealized loss on your statement. That is where tax loss harvesting comes in. You can sell the stock you bought and buy something similar for 31 days. The idea of buying something similar is because you may still want exposure to that specific area of the market. A few classic examples would be selling Coca-Cola, buying Pepsi, or selling Home Depot and buying Lowes.

Why 31 days? The IRS says that you must hold the second stock for 31 days for the tax loss you are trying to harvest to stick. Otherwise, you get what is called a wash-sale. A wash-sale eliminates the tax loss that you took when your tax reporting comes out from your broker during tax season.

There are some inherent problems with this strategy.

For one, during the 31 days you were not in the original stock, it could have shot up in price. When you try to get back into the stock you pay a higher price than you ever wanted, which is frustrating. Worst still, the name that you are in could fall or be flat during those 31 days, so you get the double whammy of having to pay more for the original stock, with less money than you originally sold it for.

Here's a quick example:

I buy 1 share of Home Depot at $100 per share, right before the stock goes down a bit, lucky me! I sell my share in Home Depot for $90 buy 1 share of Lowes at $90 per share with the goal of holding it for 31 days. I realize $10 in tax losses which is some what positive. However, during those 31 days, Lowes had a bad earnings report and went down, so now my $90 has dropped to$80, and to make matters worse, Home Depot had a stellar report, and now ittrades at $110 per share. After 31 days I sell my Lowes stock, get another $10 in tax losses, but my $80 won’t even buy 1 full share of Home Depot!!

So, I realized $20 in capital losses, and I missed out on a 10% move in Home Depot!

Additionally, since it is difficult to find companies that all do the same thing, trading multiple names within a certain area in 31 days means that you really can only tax loss harvest once or less than a handful of times within one month, which makes things tough.

Now, with the prevalence of Exchange Traded Funds, you could theoretically trade in and out of index or sector-based ETFs more frequently. The IRS has said that the provider of the ETF would be different enough to constitute a different security.

Example: Companies like Invesco, MSCI, BlackRock, State Street, Vanguard, etc. all have an ETF for the Technology sector. The underlying companies within that ETF are basically the same, but because each company is different, I could theoretically swap technology sector ETFs between companies, getting the same exposure, and being able to still ride out the market volatility without having a wash sale within 31 days.

The problem with this strategy can be easily shown below.

This chart shows SPY, an ETF that has been tracking S&P 500 since 1993. What you may notice is how much this has gone up. Yes, there have been times when the market goes down, but one of the things the stock market tends to do after making new all-time highs; it makes newer all-time highs.

Which means at some point, all the stocks that you own, or the ETFs that you own lose the ability to sell for a tax loss that you can harvest. So, if you cannot harvest any tax losses, how good is a tax loss harvesting strategy?

There are some new strategies that can take this same strategy, but also put a short position on, even for a portion of the portfolio. Let’s see how that works, from a high level.

If I have $10,000 in a portfolio of ETFs that I think will go up, but $1,000 in a similar portfolio betting that the stocks go down, this is known as having leverage and a short position on the portfolio.

In this scenario, if your portfolio goes up in value, that means that the $1,000 you have betting that the portfolio will go down would lose. Which means your $1,000 goes down in value and you could harvest those losses for your realized tax losses. So, you’re able to generate tax losses during an up market.

If, on the other hand, your $10,000 portfolio goes down in value, the $1,000 you’re betting against it would go up. So, you could not take the realized loss in the $1,000 short position (because that would go up in value) but you could take it in the $10,000 long position that has gone down.

Win-Win, right? Not exactly. To take a short position on a stock or index, you must borrow. To borrow, you need what is called margin. With margin, there is an inherent margin cost attributed to that, which is ultimately an expense and a fee drag on the overall returns.

Additionally, it is recommended that you leverage a true professional to run this strategy because there is a lot to be aware of to really execute this.

But this is something that can work.

Conclusion

You cannot (legally) avoid paying your taxes. But when managed thoughtfully,proactively, and appropriately, you can minimize, mitigate, and defer your taxes while still holding on to the gains that you have.

The biggest point in all the strategies above is being proactive. There is not much that can be done after a sale has been made and the gains have been realized. The IRS does not really allow a “do-over” if you accidentally realize a gain.

So, speak with a professional, come up with astrategy that aligns with your goals and what you want the proceeds to go towards, and figure out what is right for you.

If you need some ideas, strategies, or want to speak further about any of the above; please reach out to us here at HUDSONPOINT capital, we would love to help you put the pieces of your puzzle together.

The opinions expressed are those of HUDSONPOINT capital and not those of Arete Wealth.

Please note that any investment involves risk including loss of principal. This is for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation of any products or services. Opinions are subject to change with market conditions. The views and strategies may not be suitable for all investors and are not intended to be relied on for legal or tax advice.

Securities offered through Arete Wealth Management, LLC, members FINRA and SIPC. Investment advisory services offered through Arete Wealth Advisors, LLC an SEC registered investment advisory firm.

.png)