Within 96 hours in May 2026, three events defined the year's IPO calendar. On May 18, a federal jury rejected Elon Musk's long-running lawsuit against Sam Altman and OpenAI, clearing the runway for OpenAI's listing. On May 20, SpaceX filed its public S-1 with the SEC. Two days later,OpenAI followed suit.

It's the closest thing to a heavyweight fight Wall Street has seen in years, and it’s no surprise that the financial press has framed it as Musk vs. Altman, Round Two.Two former co-founders turned bitter rivals, competing at the highest level and on the largest stage to dominate AI, heading to public markets simultaneously and aiming for valuations above $1 trillion per company.

It’s a headline-maker, for sure. But the more useful framing for pre-IPO investors is a bit different. SpaceX and OpenAI are not substitutes for each other. They are different businesses, with different revenue profiles, governance structures,and thesis that may (or may not) justify the price tags.

The question isn't really “Which one wins?” The goal is to understand what each company is,what it does, and how it fits (or doesn't) into a portfolio.

Read more:

The SpaceX IPO: The Largest Listing in History

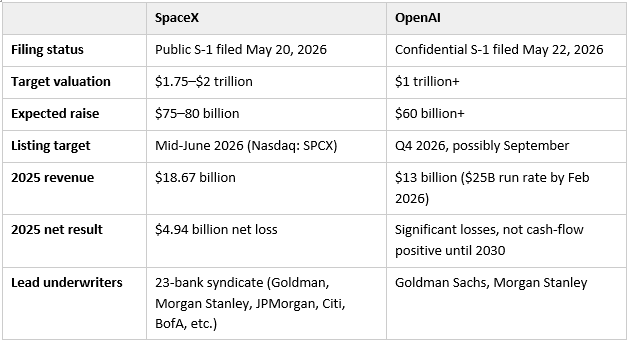

The Companies at a Glance

While both companies would rank among the largest IPOs in history. SpaceX, if priced as expected, would be the largest IPO ever. But the businesses behind those valuations are doing very different things.

Sources: SpaceX S-1, Al Jazeera, Yahoo Finance, CNBC, TechCrunch, Sacra

Hard Infrastructure vs. Software Platform

Let’s start with SpaceX. The recently filed S-1 breaks SpaceX into three business lines:

- Connectivity (Starlink) generated $11.4 billion of the company's $18.67 billion in 2025 revenue — about 61% of the top line —and roughly $4.4 billion in operating profit at an EBITDA margin of approximately 63%.

- The Space segment (Falcon, Dragon, Starship) generated $4.1 billion in revenue but posted an overall operating loss.

- The AI segment (xAI), newly acquired and consolidated as of February, lost $2.47 billion in Q1 2026 alone.

Strip away the headlines, and SpaceX is largely a satellite internet company, with Starlink currently subsidizing everything else. Its subscriber base reached 10.3 million customers across 160+ markets by Q1 2026, nearly doubling year over year. Financially, Starlink behaves more like a high-margin software platform than a traditional aerospace business.

That being said, per-user economics are softening, with ARPU sliding from around $99 in 2023 to about $66 by Q1 2026 as Starlink expands into lower-priced international markets.

Meanwhile, OpenAI looks very different. There is no cash-generating segment carrying the weight of unprofitable bets, so the entire company is at stake.

OpenAI hit roughly $25 billion in annualized revenue by February,growing at a pace several outlets have called unprecedented in enterprise software (3x per year sustained at a multi-billion-dollar scale). Notably,enterprise revenue now accounts for more than 40% of the mix and is projected to reach parity with consumer revenue by the end of 2026.

But the company is burning capital at an extraordinary rate. Adjusted gross margins fell to roughly 33% in 2025 as inference costs quadrupled. Cash burn is projected at $25–27 billion in 2026 and up to $63 billion in 2027. OpenAI is not expected to turn cash-flow positive until 2030.

Founder Control vs. Public Benefit

The Musk-vs.-Altman framing makes for good content, but what are they actually doing with these massive companies?

- SpaceX is a controlled company: Per the S-1, Musk holds

- of post-IPO voting power through a dual-class share structure in which Class B shares carry 10 votes each to ClassA's 1. He'll continue as CEO, CTO, and chairman simultaneously. Under controlled-company status, SpaceX is exempt from Nasdaq rules requiring a majority-independent board. Shareholder proposals require ownership of at least $1 million in shares or 3% of total outstanding shares, and disputes must be resolved through mandatory arbitration. In short, public shareholders will own equity in SpaceX but will have effectively no influence over how it's run.Three public pension funds, including CalPERS, have already protested the structure.

- OpenAI is something else entirely: Following its October 2025 restructuring, the company going public is OpenAI Group PBC, a public benefit corporation legally obligated to balance commercial returns with its stated mission. The PBC is controlled by the OpenAI Foundation, a nonprofit with eight independent directors, including Altman, who holds a roughly $130 billion equity stake. Microsoft holds 27%, or around $135 billion. According to a reconstructed cap table circulated in April 2026, Altman himself is listed as holding no or pending equity in the companyhe runs.

Both structures concentrate control, but at opposite ends of the spectrum. At SpaceX, all power is concentrated in one founder. At OpenAI, control sits with a foundation whose mission isn't shareholder return (and whose board has fired its CEO once before, in November 2023).

The IPO Trajectory: State of Play

Both companies are heading to public markets in 2026, but they're at very different points in the process. Here's where each stands today:

- SpaceX is further along with its public S-1: The roadshow window opens 15 days after public filing, and a mid-June 2026 IPO has been widely reported. Unsurprisingly, 23 banks are underwriting the deal, led by Goldman Sachs, Morgan Stanley, Citi group, JPMorgan, and BofA Securities. Retail investors will be able to participate at the IPO price through Schwab,Fidelity, Robinhood, SoFi, and E*TRADE, an unusual choice for a deal this large(and a deliberate one).

- OpenAI's timeline is less certain: The confidential filing means the prospectus stays private until approximately 15 days before the public roadshow. Reporting anticipates a Q4 2026 listing, possibly as early as September, with Goldman Sachs and Morgan Stanley leading the underwriting. But OpenAI's own CFO has reportedly suggested a 2027 listing may be more realistic. A delay would not be surprising, given the complexity of the PBC structure,financial audits, and ongoing disputes over the Microsoft revenue-sharing arrangement.

3 Key Takeaways for Interested Pre-IPO Investors

1. SpaceX and OpenAI are not substitutes

The companies are exposed to fundamentally different opportunities and risk vectors. SpaceX is currently a maturing satellite internet business with optionality on Starship and orbital AI compute. OpenAI is exposed to both B2B and B2C competition and pressures,with material capital intensity and a longer runway to profitability.

2. The valuation math is built on different timelines

SpaceX's valuation is tied to Starlink's recurring revenue, the Starship commercialization roadmap, and operational milestones. But there’s already cash flow, and a lot of it. OpenAI's valuation is tied to a revenue trajectory that must continue to grow at an extraordinary rate while compute costs ease. Both are aggressive, but they reward and punish different things, on different timelines.

3. Key-person and governance risk show up differently

At SpaceX, the entire decision-making structure runs through one person who oversees four operating companies (Tesla, SpaceX, X, and xAI). At OpenAI, the CEO serves on a boardwhere eight independent directors hold a majority. But this was the same structure that led to his 2023 firing. Public-market investors will be pricing a control structure either way.

The Pros and Cons of Pre-IPO Exposure

Pre-IPO access is available today through secondary-market platforms, structured vehicles, and select private-market funds. But investors should stay clear-eyed about the trade offs:

- Illiquidity: Pre-IPO positions cannot be freely sold. Holding periods are uncertain and depend on whether and when an IPO proceeds.

- Valuation risk: A delay, missed revenue milestone, or broader market correction could reset private valuations before any listing occurs.

- Limited financial transparency: While SpaceX's S-1 is now public, OpenAI's financials remain largely based on third-party estimates until the confidential filing is made public.

- Concentration and governance risk: As covered above, the structural risks at both companies are real and apply with full force in private markets, where there is less recourse.

- Access restrictions: Pre-IPO investment in either company is generally limited to qualified investors and, in many cases, qualified purchasers.

How HUDSONPOINT capital Seeks To Provide Access to Pre-IPO Opportunities

It cannot be understated that pre-IPO investing is not suitable for all investors. But for those with the right risk profile, time horizon, and broader portfolio context,it can offer access to companies at private-market prices before public markets reset them.

HUDSONPOINT capital provides clients with access to private-market opportunities typically unavailable to individual investors. Our approach includes:

- Rigorous screening and due diligence on every opportunity we present

- Risk-adjusted portfolio design that considers how pre-IPOs interact with your existing holdings

- Clear education and transparency around the specific risks of private securities

If you're interested in understanding whether pre-IPO exposure to SpaceX, OpenAI, or other high-profile private companies fits yourportfolio, HUDSONPOINT capital advisors are here to help you evaluate these opportunities and explore available investment options.

The opinions expressed are those of HUDSONPOINT capital and not those of Arete Wealth.

Please note that any investment involves risk including loss of principal. This is for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation of any products or services. Opinions are subject to change with market conditions. The views and strategies may not be suitable for all investors and are not intended to be relied on for legal or tax advice.

Securities offered through Arete Wealth Management, LLC, members FINRA and SIPC. Investment advisory services offered through Arete Wealth Advisors, LLC an SEC registered investment advisory firm.

.png)

.png)