A major set of tax and policy changes officially takes effect under the “One Big Beautiful Bill.” These provisions reshape the tax landscape that investors, families, and business owners have been preparing for over the last several years. For wealth management clients, understanding what is changing— and how those changes affect planning decisions — is critical.

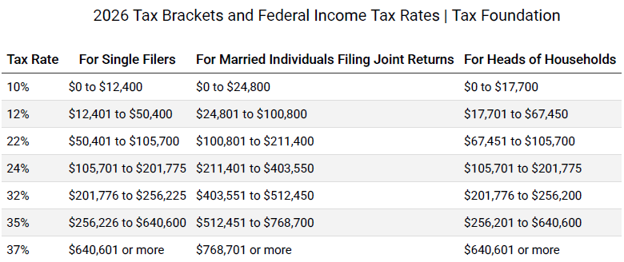

1. Individual Tax Rates and Deductions Become the New Normal

One of the most consequential aspects of the legislation is the permanent extension of the current individual tax bracket structure. Without legislative action, many taxpayers would have faced higher marginal rates beginning in 2026.

Key impacts:

- Current tax brackets remain in place, reducing the risk of sudden tax increases

- Standard deductions remain elevated and continue to adjust for inflation

- Many households retain higher after-tax cash flow compared to pre-2026 rules

From a planning perspective, this may help create more certainty around long-term income strategies, Roth conversions, and retirement distribution planning. While rates are stabilized, income thresholds and deductions still warrant annual review to avoid bracket creep.

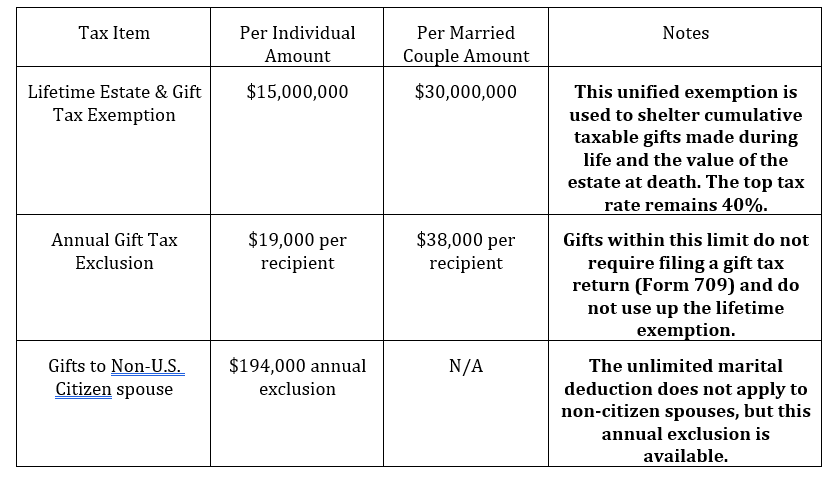

2. Estate and Gift Tax Exemptions Expand Planning Flexibility

The federal estate and gift tax exemption increases again in 2026 and is indexed for inflation, preserving a higher level of wealth transfer flexibility.

What this means for families:

- More assets can pass to heirs without federal estate tax exposure with proper planning

- Lifetime gifting strategies may offer enhanced planning opportunities when implemented with appropriate professional guidance

- Trust and legacy plans may be restructured when necessary

Clients who delayed gifting or estate planning due to uncertainty now have clarity. However, this does not eliminate the need for planning — state estate taxes, beneficiary structures, and long-term family goals remain central considerations.

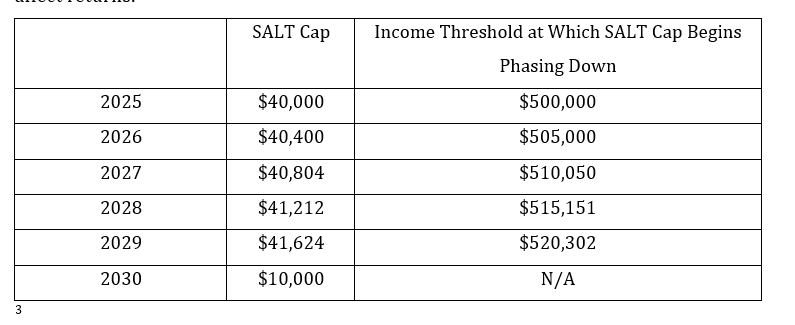

3. SALT Deduction Relief Changes the Math for High-Tax States

The legislation modifies the state and local tax deduction limits beginning in 2026, particularly benefiting taxpayers below certain income thresholds.

Why this matters:

- Higher deductibility of state and local taxes for qualifying households

- Reduced tax drag for clients in high-tax states when structured properly with the guidance and partnership of a trusted tax advisor

- Planning opportunities around timing of income and deductions

This change could result in improved after-tax returns for affected clients,but benefits may phase out at higher income levels. Strategic income management becomes increasingly important. Keep in mind that fees associated with investments also can affect returns.

4. Charitable Giving Becomes More Accessible

A notable change allows taxpayers who take the standard deduction to still receive a limited tax benefit for charitable contributions.

Planning implications:

- Charitable giving may provide tax benefits for certain households, depending on individual circumstances and proper structuring

- Donor-advised fund strategies may need reevaluation

- Philanthropy can be better aligned with cash-flow planning when done appropriately

This provision may help broaden the role of charitable planning beyond high-income itemizers and allows advisors to integrate philanthropy into a wider range of client strategies where appropriate.

5. Targeted Benefits for Retirees and Older Investors

Several provisions taking effect in 2026 are designed to support retirees and near-retirees.

These include:

- Additional deductions or income offsets for individuals over a certainage

- Expanded health-related savings opportunities

- Improved coordination between retirement income and tax planning in most cases

For retirees, this reinforces the importance of coordinated withdrawal strategies across taxable, tax-deferred, and tax-free accounts.

6. Broader Planning Considerations Beyond Income Taxes

While income and estate taxes draw the most attention, the legislation also influences longer-term financial planning:

- Changes to health savings rules affect retirement healthcare strategies

- New reporting and compliance rules may impact business owners and cross-border families

These elements reinforce the value of proactive, integrated financial planning rather than reactive tax filing.

Final Thoughts: Planning in a More Certain, But Still Complex, Environment

The 2026 changes under the One Big Beautiful Bill bring welcome stability to the tax code, but stability does not eliminate complexity. The opportunity now lies in thoughtful planning rather than last-minute adjustments.

Key priorities for clients:

- Update tax projections using 2026 rules

- Revisit estate and gifting strategies

- Review charitable and deduction planning

- Coordinate retirement income with the new tax framework

Whenever conducting there views and planning discussed above clients need to keep a few additional things in mind. First, all government related items are subject to change, so putting a plan in place for generational gifting, taxes, etc. should all be done in concert with a professional. Specifically, a trust Tax advisor, Trust & Estate Planning Attorney, and Financial Planner to ensure that all the goals and outcomes align with current tax code. As tax policy may change, having a partner to ensure future alignment is highly recommended.

The state level is also, at times, different than the federal level in terms of tax, gifting, and Estate expenses. The partnership with a tax advisor or CPA is highly recommended to ensure you are doing everything you can to align and take advantage of your next steps.

In an environment of greater clarity, informed decisions — not assumptions — may help drive better long-term outcomes.

Any questions, comments, or feedback are always welcome. Please reach out to us at HUDSONPOINT capital we look forward to hearing from you.

The information provided in this blog is for general informational purposes only and does not constitute tax, legal, or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction.

The opinions expressed are those of HUDSONPOINT capital and not those of Arete Wealth.

Please note that any investment involves risk including loss of principal. This is for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation of any products or services. Opinions are subject to change with market conditions. The views and strategies may not be suitable for all investors and are not intended to be relied on for legal or tax advice.

Securities offered through Arete Wealth Management, LLC, members FINRA and SIPC. Investment advisory services offered through Arete Wealth Advisors, LLC an SEC registered investment advisory firm.

.png)